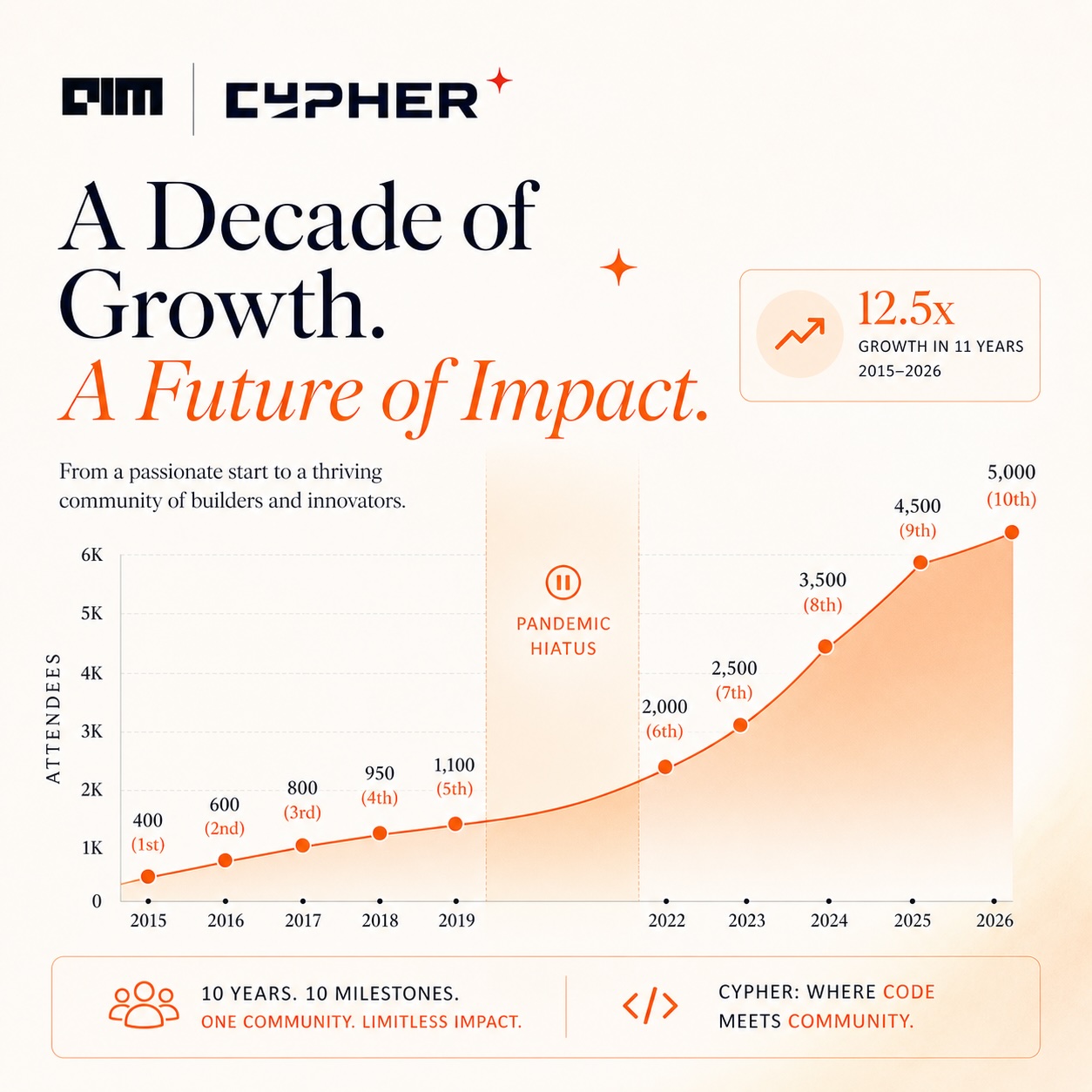

In September 2015, four hundred people gathered at a hotel in Bengaluru to attend the first Cypher. The agenda was modest by today’s standards: a main ballroom for keynotes and panels, two parallel workshop tracks, 32 speakers, and a recurring debate that ran through the corridors — whether India needed more “business storytellers” who could translate analytics into action, or whether the field was producing too many storytellers and not enough builders.

In October 2026, Cypher’s tenth edition will host more than 5,000 attendees, 150-plus speakers, and 100-plus exhibitors across three days at KTPO Whitefield. The agenda spans agentic architecture, MLOps at scale, sovereign AI infrastructure, and the governance scaffolding for autonomous systems in regulated industries. The “business storyteller” debate is gone. It has been replaced by a more uncomfortable one: whether Indian enterprises are building durable AI capability or assembling expensive demos that will collapse the moment a foundation model upgrade breaks the workflow.

This is not a story about how a conference grew. Conferences grow. This is a story about what an honest reading of one event’s evolution reveals about the country it serves — and where the rhetoric and the reality have stopped matching.

Call it the Cypher Index.

Figure 1: Cypher attendee growth across 10 editions. Source: AIM, with figures for select years approximate.

The premise

Conferences are confessional documents. The themes that get keynote billing, the sponsor categories that buy expo footprint, the job titles that fill the audience, the questions that get asked from the floor — these are the field’s tells. They reveal what a market believes about itself, what it is willing to pay to learn, and what it is quietly anxious about.

Cypher is uniquely positioned to read this signal in India. It has run every year since 2015 (with a two-year pandemic interruption between editions five and six). It has indexed its agenda to whatever the market was willing to pay attention to in that twelve-month window. It has not pivoted, rebranded, or chased a different audience. The brand has been a constant variable, which means the changes inside the brand carry meaning. For the wider context on AIM’s editorial coverage of Indian AI, see Analytics India Magazine and AIM Research.

What follows is not a victory lap. It is an attempt to read the index against the country’s actual AI maturity — and to flag the gaps where the conference has moved faster than the enterprises it serves, and where it has moved slower.

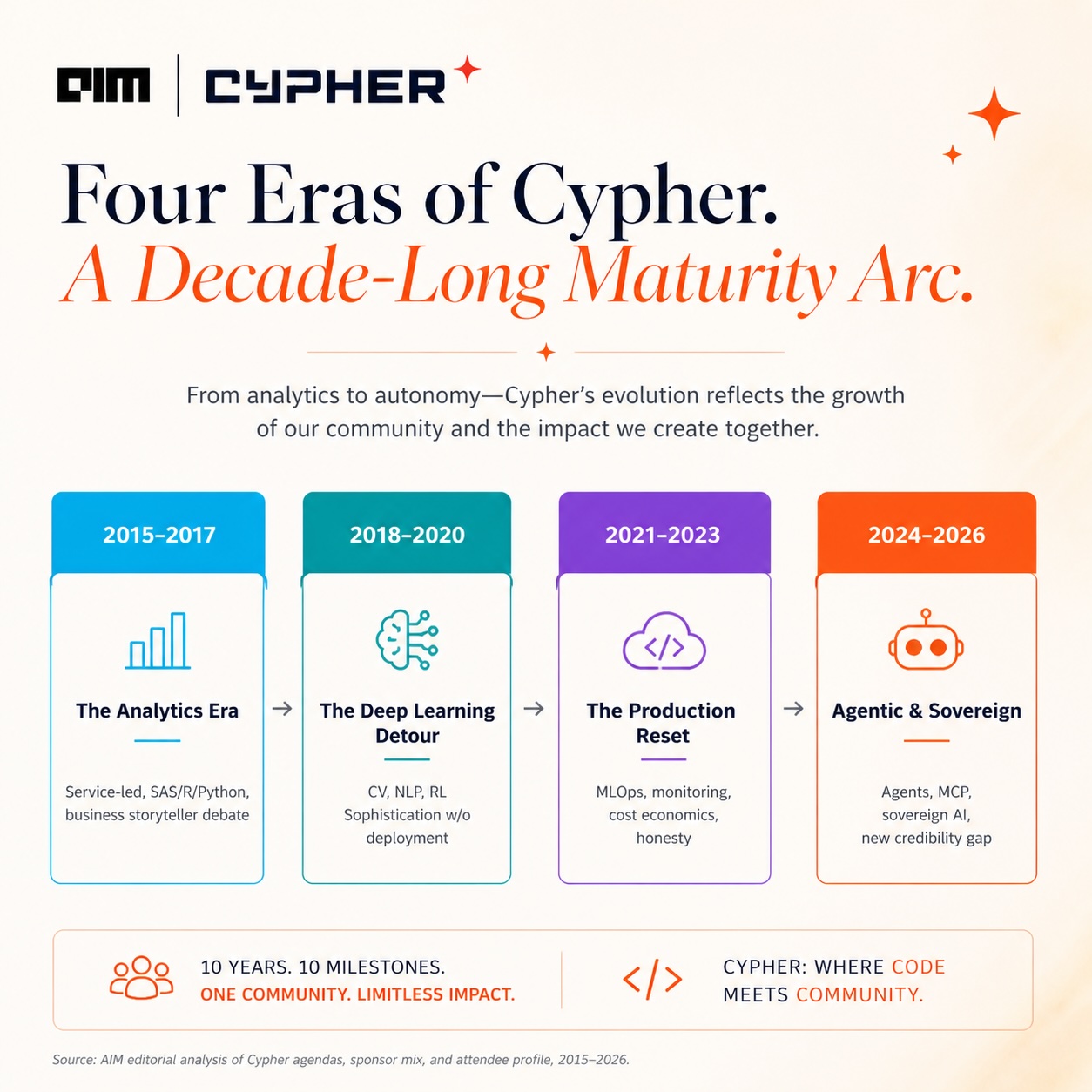

Figure 2: The four editorial eras of Cypher, 2015–2026.

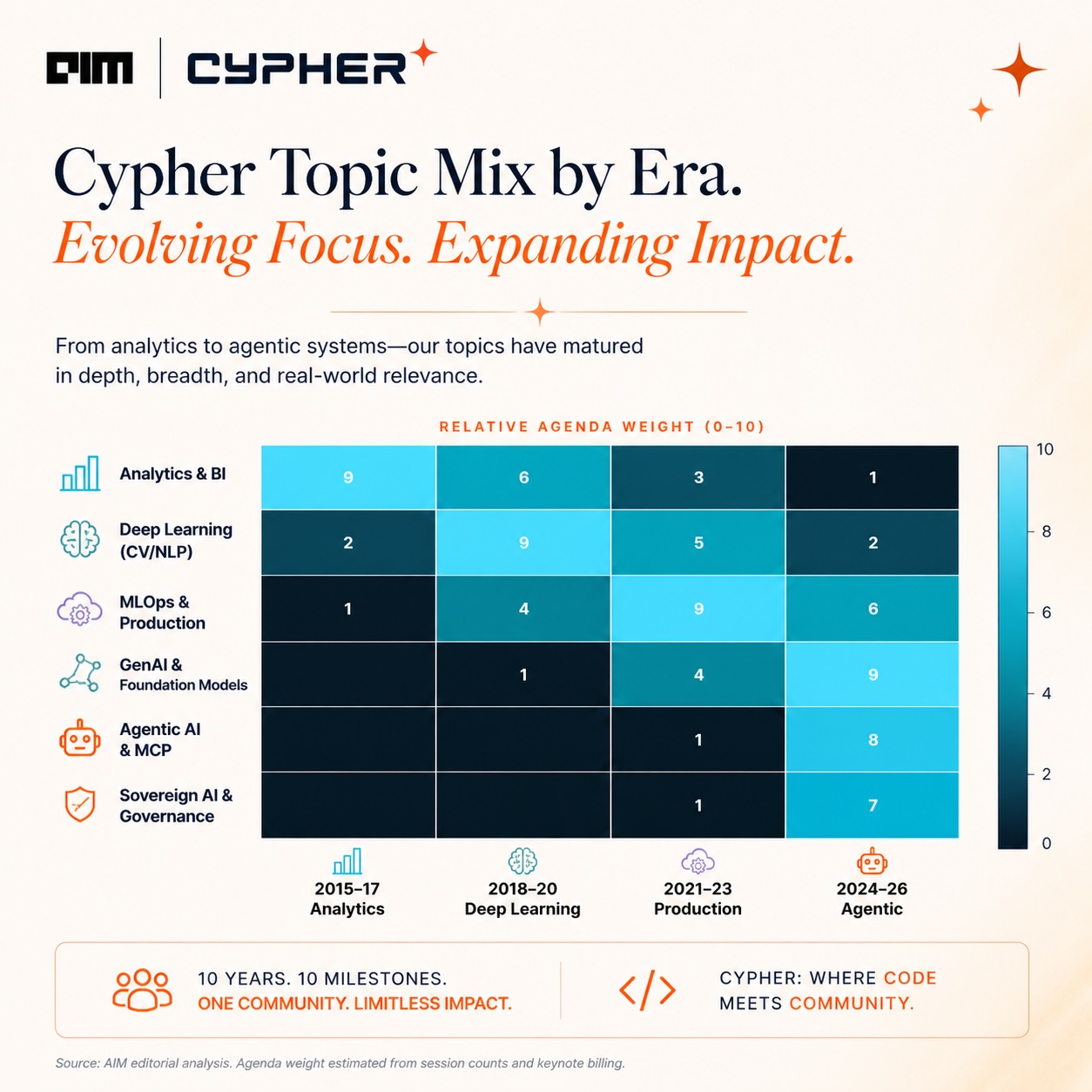

Era one (2015–2017): the analytics era — when “data science” was an aspiration, not a function

The first three Cyphers were dominated by service-led analytics narratives. The dominant sponsor category was the consulting firm with an analytics practice. The dominant attendee was the analytics manager at a Fortune 500 captive in Bengaluru, Hyderabad, or Pune. The dominant tool conversation was around SAS, R, and the early arrival of Python.

The maturity signal: India had analytics talent but very little of it sat inside enterprises. It sat inside service companies that sold analytics work to enterprises in the US and UK. The country was an outsourcer of intelligence, not a consumer of it.

The rhetoric of the era was about democratisation — making analytics accessible, building self-service dashboards, producing the now-mythical 100,000 data scientists India was supposedly going to need. The reality was a market structure where the analytics function lived two layers removed from the business, and where enterprise leaders had not yet decided whether data was a strategic asset or an IT cost.

What Cypher’s agenda revealed in this era, retrospectively, was a market that had skill but no demand-side maturity. The buyers were not yet buyers.

Era two (2018–2020): the deep learning detour — sophistication without deployment

The middle period of Cypher tracked the global deep learning wave. By 2019, the conference’s fifth edition had 1,100 attendees, 100 speakers, and 70 talks. Sessions on computer vision, NLP, and reinforcement learning crowded the agenda. Sponsor mix shifted — cloud providers entered prominently, GPU vendors made first appearances, and the consulting firms began rebranding their analytics practices as AI practices.

This was the era when the gap between Indian enterprise rhetoric and Indian enterprise practice opened wide. CXOs commissioned AI strategies. Boards demanded AI roadmaps. The press released the words “AI-first” and “AI-led” with no friction. And meanwhile, on the ground, very few production AI systems existed inside Indian enterprises that could not have been built with a SQL query and a regression model.

Cypher’s agenda in this era was sophisticated. The country’s actual deployments were not. The conference was three to five years ahead of the buyer.

The maturity signal here is uncomfortable: India produced an enormous amount of AI talk in this era and a small amount of AI work. The two-year pandemic gap that interrupted Cypher between 2019 and 2022 was, in retrospect, useful. It forced the market to either deploy what it had been talking about or admit it had not been deploying.

Most enterprises picked the third option, which was to wait.

Era three (2021–2023): the production ML reset — when the conversation got honest

Cypher’s return in 2022 came after the two-year hiatus, and the agenda had shifted in a way that took the field by surprise. The fashionable topics of 2019 — GANs, transfer learning, custom architectures — had given way to harder, less glamorous concerns: MLOps, data quality, model monitoring, drift detection, vendor lock-in, and the cost economics of running ML in production.

This was Cypher’s most editorially honest era. The conference had stopped pretending the country was at the frontier. It was instead asking, with some urgency: how do we make the AI we already have actually work? The 7th edition in 2023 deepened this thread.

Sponsor mix in this period reflects the shift cleanly. Vector database companies appeared. Observability platforms appeared. Data quality vendors appeared. The cloud hyperscalers doubled their footprint. The consulting firms shifted their messaging from “AI strategy” to “AI implementation.” Job titles in the audience changed too — “Head of MLOps” and “ML Platform Engineer” began outnumbering “Data Science Manager.”

The maturity signal: India’s AI conversation had finally caught up with its AI deployments, and both were now operating at the level of “production basics.” This was less exciting than the deep learning era. It was also, for the first time, real.

What this period revealed about the country was not flattering, but it was true. India’s AI maturity in 2022 and 2023 was at roughly the level the United States and Europe had reached in 2018 and 2019 — about three to four years behind, depending on the vertical. Banking and financial services were ahead. Manufacturing and public sector were further behind. Retail was bimodal — a handful of leaders, a long tail of laggards.

Era four (2024–2026): the agentic and sovereign era — and the new credibility gap

Cypher’s most recent three editions have been shaped by two parallel forces: the generative AI explosion and the sovereign AI question.

The GenAI track in Cypher’s agenda has expanded faster than any topic in the conference’s history. From a handful of sessions in 2023, it now spans entire days. Agent architectures, MCP integration, RAG systems, foundation model fine-tuning, prompt engineering as a discipline, AI safety, and governance frameworks — these are no longer adjacent topics. They are the centre of gravity.

The sovereign AI conversation, by contrast, is newer and more contested. India’s compute infrastructure question, the IndiaAI mission’s GPU allocation, the rise of Indian foundation models, the geopolitics of AI supply chains — these are agenda items at Cypher 2026 that did not exist at Cypher 2023.

Sponsor evolution in this era is the most revealing yet. Indian sovereign cloud players have appeared. Foundation model companies — global and Indian — are now keynote sponsors. Agentic platform vendors have emerged as their own category. The consulting firms are now selling “agent transformation” the way they were selling “digital transformation” a decade ago.

But here is the uncomfortable observation that Cypher’s agenda is forcing into the open in 2026: India’s enterprise AI maturity has improved, but the gap between what gets discussed and what gets deployed has reopened. The country talks about agents at frontier-lab sophistication. It deploys, mostly, chatbots with RAG layers that fail when the underlying model is upgraded.

This is not unique to India. Every market is grappling with this gap. But the gap matters more in India because the local AI narrative is built on the assumption that the country is positioned to lead, and the deployment data does not yet support that narrative.

Figure 3: Topic mix evolution across the four eras. Editorial estimate of agenda weight from session counts and keynote billing.

What the Cypher Index actually tells us

Read across ten editions, four patterns emerge.

One: the conference has consistently led the market by 18 to 36 months. Topics that appear at Cypher in year N show up in Indian enterprise budgets in year N+2 or N+3. This was true of cloud-based ML, of MLOps, of vector databases, and is currently playing out for agentic systems. If the pattern holds, the agentic deployments most Indian enterprises will treat as cutting-edge in 2028 are being demonstrated at Cypher 2026 today.

Two: every era has had a credibility gap, and the gap has changed shape but not closed. In era one, the gap was talk-versus-skill. In era two, the gap was skill-versus-deployment. In era three, the gap closed briefly. In era four, it has reopened — talk-versus-production, frontier-aspiration-versus-enterprise-reality. This gap is the country’s defining AI characteristic and it has not yet been seriously addressed by either policy or industry.

Three: the buyer profile has matured faster than the seller profile. The Cypher attendee in 2026 is a more sophisticated buyer than the Cypher attendee in 2019 — more questioning, more deployment-oriented, less impressed by demos. The vendor pitches, by contrast, have not evolved at the same rate. There is still too much “AI-powered” marketing language and too little hard talk about reliability, cost, and integration.

Four: the country’s AI talent base has gone from being concentrated in service companies to being distributed across enterprises, startups, and frontier labs — but the distribution is uneven. A small number of Indian enterprises now have genuinely production-grade AI capabilities. A small number of Indian startups are building globally competitive AI products. A small number of Indian engineers are working at frontier labs. The rest of the market is still catching up, and the spread between leaders and laggards has widened, not narrowed.

The next index reading

If Cypher’s agenda is a forward indicator, the topics that are emerging at the edges of the 2026 conference are worth watching. Sovereign AI infrastructure as a procurement decision, not a policy debate. AI governance as an enterprise function with budget and headcount. The economics of agent deployment — cost per task, reliability per dollar, total cost of autonomy. The talent shift from prompt engineers to forward-deployed engineers. And, quietly but unmistakably, the question of whether India’s enterprise AI strategy will be built on imported foundation models or domestic ones.

These will be the dominant conversations at Cypher 2027 and 2028. They will become enterprise budget decisions in 2029 and 2030. The maturity curve will continue to bend, but the credibility gap — talk versus production — will define whether India is genuinely an AI-led economy by the end of the decade or merely an AI-loud one.

A conference cannot answer that question. But it can, year after year, tell us with uncomfortable clarity which way the curve is bending. Ten editions in, the Cypher Index suggests the country is further along than its sceptics claim and further behind than its boosters allow — which is, on balance, a more honest place to be than it has been at any point in the past decade.