Finance is the canary in every technology coal mine. The sector has regulators, risk teams, quarterly disclosure obligations, and a deep institutional muscle memory of what happens when a model breaks in production. If banks, insurers, and asset managers are deploying a new technology in revenue-touching workflows, that is a signal the technology has crossed a maturity threshold. If they are still asking whether it is real, the maturity is not there yet.

This is what makes the Indian BFSI presence on the Cypher stage, year over year, such a useful index. The questions asked, the speakers chosen, the deployments described — read together, they form a four-year arc that maps almost perfectly to the global trajectory of enterprise GenAI. Indian finance moved from sceptical observation in 2022, to cautious exploration in 2023, to validation in 2024, to actual production deployment in 2025.

Twenty-three named BFSI deployments appeared on the Cypher stage between 2023 and 2025. The pattern across them is the most important deployment story in Indian enterprise AI — and the one least understood outside the sector itself.

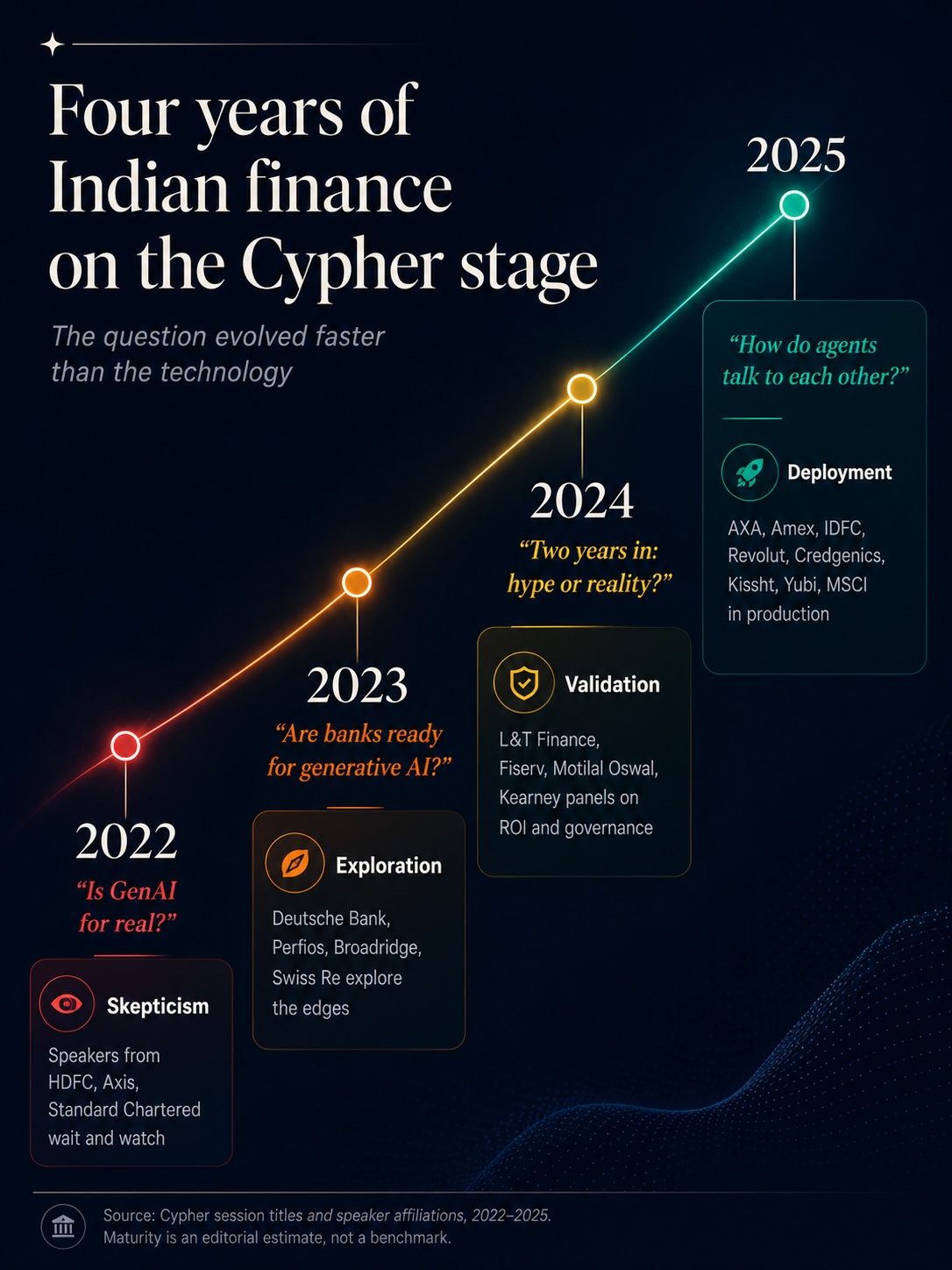

Figure 1: The four-year question arc of Indian finance on the Cypher stage, from skepticism in 2022 to production deployment in 2025.

2022: The skepticism phase

When Cypher returned in-person in 2022 after the pandemic, the Indian BFSI presence was substantial but cautious. Past speakers and attendees from the era included HDFC Bank, Axis Bank, Standard Chartered, Wells Fargo, and Bharti AXA. The conversation was about the next wave of analytics rather than generative AI specifically — ChatGPT was still six weeks away from launch when Cypher 2022 opened.

What was being discussed: machine learning at scale, fraud detection, predictive analytics in lending, model governance in risk. What was not being discussed: large language models, retrieval-augmented generation, or anything that resembled the GenAI conversation that would dominate every subsequent edition. The 2022 BFSI participation was the last edition where Indian finance came to Cypher to learn about traditional ML rather than to grapple with the implications of generative models.

2023: The exploration phase

Cypher 2023 was the first edition where GenAI was the centre of gravity in BFSI sessions. The most consequential session was Srikanth Gopalakrishnan’s, from Deutsche Bank, simply titled “Are banks ready for generative AI?” That question framed the entire year.

Around it, a cluster of BFSI speakers explored the edges. Sabyasachi Goswami from Perfios spoke on “Generative AI’s Multifaceted Role in Fintech.” Sheenam Ohrie from Broadridge spoke on “Generative AI for designing FinTech products and solutions.” Vivek Pandyarajan from Swiss Re asked about “preparing to coexist with Generative AI” — the careful framing of a reinsurance executive who knew that any production deployment would face regulatory scrutiny.

Other 2023 BFSI participation was characteristically wide-ranging. Ashutosh from Cigna covered AI in health insurance. Pancham Taneja from Delta Capita explored AI and blockchain. Ravi Variar from Morningstar discussed NLP in large data pipelines. Abhishek Choudhary from MathWorks tackled climate risk management in financial services. A panel on “Leveraging Quant Modeling & AI with Model Governance Insights” ran with Prashant, Arpit, and Rahul as panellists.

The unifying characteristic of the 2023 BFSI agenda was its tentativeness. Almost every session title is framed as a question or an exploration. None of them describe a production system. The sector was probing the technology at the edges of its operations, not yet putting it in the centre.

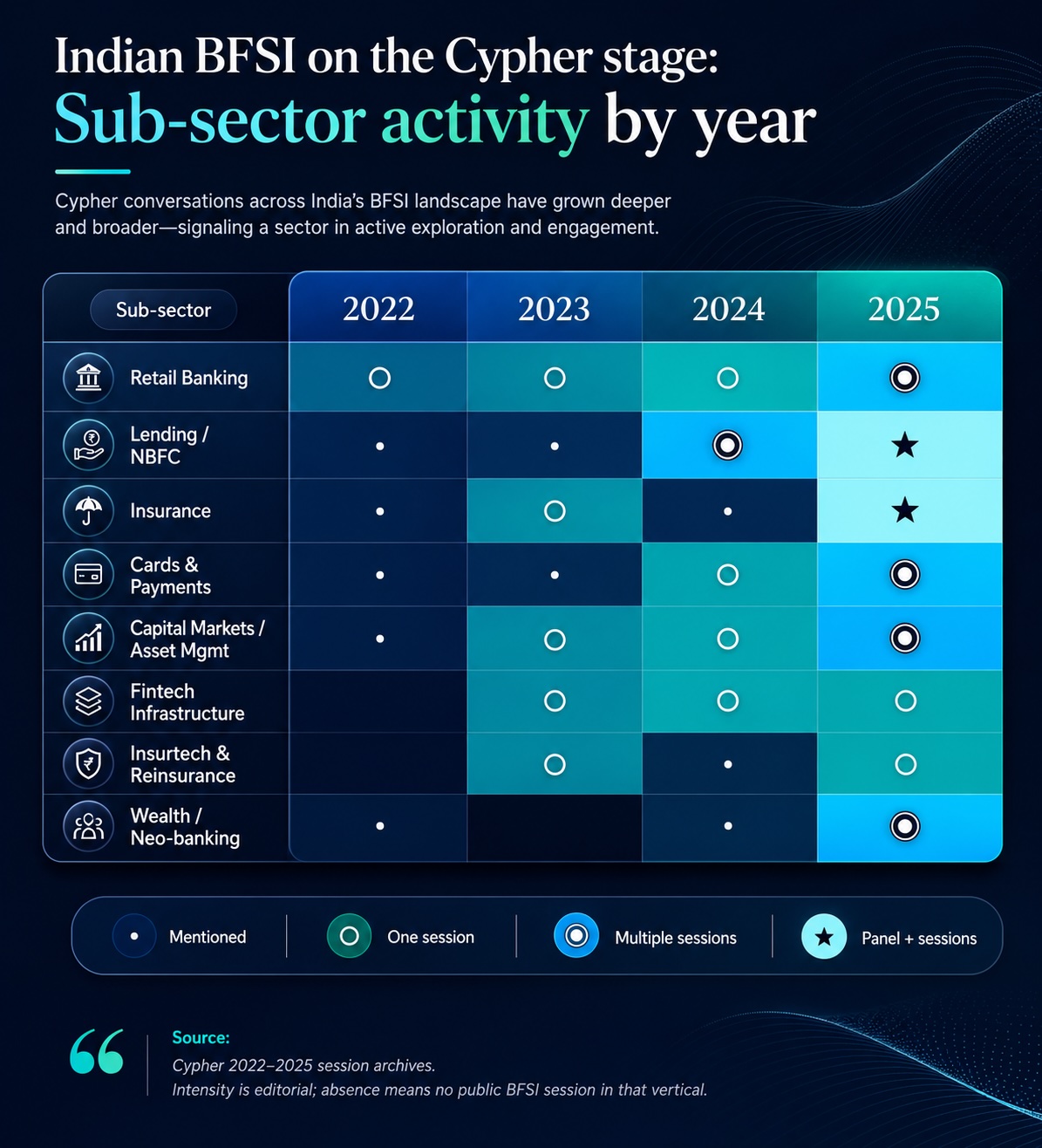

Figure 2: Indian BFSI sub-sector activity by edition. Lending and insurance saw the steepest 2024–2025 jump from single sessions to panel-level participation.

2024: The validation phase

Cypher 2024 was the year Indian finance stopped exploring and started measuring. The flagship session of the year, from this sector’s perspective, was a panel titled “Two Years of Generative AI: Evaluating the Hype and Reality” — the explicit acknowledgment that the moment for hype had passed and the moment for evidence had arrived.

The named BFSI deployments at 2024 were concrete in a way they had not been the previous year. Debarag Banerjee from L&T Finance presented “How AI will change the business of lending” — not as speculation but as a description of changes underway. Sumeet Tandure from Snowflake spoke about how GenAI was overtaking traditional ML in financial services. Maksim Khaitovich from Kearney delivered “Measuring what works in AI: Kearney’s Business First Approach to LLM Leaderboards.”

The 2024 wall also featured the first explicit governance sessions of the BFSI arc. “Responsible AI: Building An Ethical Governance Framework for AI Models in BFSI” ran as a dedicated session. “AI in Fintech: Striking the Right Balance Between Rapid Innovation and Sustainable Growth” anchored a panel. The signature shift of 2024 is that BFSI speakers stopped asking whether GenAI would work and started asking how to deploy it responsibly. That shift is the deepest signal of category maturity available in conference programming.

Fiserv’s VP of Innovation and Intelligent Automation appeared on the speaker list. Motilal Oswal’s EVP and Head of Data Science took the stage. American Express’s VP of Credit and Fraud Risk participated. None of these are speculative speakers. They are the people who run live AI systems inside large financial institutions, and their presence at Cypher 2024 was a statement that those systems now existed.

2025: The deployment phase

Cypher 2025 was the year the Indian BFSI sector showed up in production. The breadth and specificity of the named deployments is the strongest single-edition evidence of category maturity in the entire decade-long Cypher arc.

Sayandeep Majumder from AXA gave two sessions — “How AXA Is Transforming Insurance with AI” and “Revolutionising Insurance: One Agent at a Time.” Both described live, scaled deployments. Himanshu Sharad Bhatt from American Express presented “Gen AI Transforming Document Intelligence” — not a pilot, a production system. Ekta Shah from MSCI tackled “GenAI in Finance: Trust, Transparency and High-Stakes Decisions.” Neha Shivran, Co-founder of Kissht, spoke on “ML for Real-Time Credit Risk Management.”

The lending sub-sector saw the most concentrated activity. Anand Agrawal from Credgenics presented “Powering the paradigm shift in debt collection with AI.” Gaurav Kumar and Vivek Srikantan from Yubi led a session titled “Can AI in Collections Be Both Efficient and Empathetic?” Three Indian fintech lenders, three different angles on the same workflow, all describing deployments in production. The collections use case is now one of the most thoroughly deployed GenAI applications in Indian financial services.

Banking-side, Shubham Agnihotri from IDFC FIRST Bank delivered “Mastering A2A: How AI Agents Talk to Each Other” — one of the first explicitly agentic banking sessions on a major Indian stage. Paroma Chatterjee, CEO of Revolut India, spoke about “Building a Borderless Bank in a Fragmented Market.” Srivatsa Subbanna, SVP and Head of Intelligent Automation and AI at Axis Bank, participated in the formal sovereign-AI debate. Banking presence on the Cypher stage in 2025 was no longer a single speaker per institution — it was multiple, senior, and operationally specific.

AXA itself took the gold-tier sponsor slot at Cypher 2025. The insurance company that asked careful questions through 2023 was, two years later, sponsoring the conference and presenting its production AI work. That trajectory — from question to sponsorship — is the cleanest single-company case study of the four-year arc.

Figure 3: Twenty-three named Indian BFSI deployments on Cypher’s stage between 2023 and 2025. Border colour indicates edition.

Seven verticals, one pattern

Read across the named deployments, the Indian BFSI GenAI adoption is concentrated in seven sub-verticals, each with its own maturity profile.

Lending and NBFC — the deepest deployment. Three named 2025 deployments (Credgenics, Kissht, Yubi) and the L&T Finance 2024 anchor. Use cases span debt collection, credit risk modelling, and underwriting empathy. This is the sub-sector where Indian fintech moved fastest, in part because it was less encumbered by legacy systems than traditional banking and in part because lenders are more comfortable with model-driven decision making.

Insurance and reinsurance — the steepest maturity climb. From Swiss Re’s 2023 “preparing to coexist” to AXA’s 2025 “one agent at a time” in two years. Indian insurers, with their compliance discipline and structured underwriting processes, turned out to be unexpectedly good first adopters of agentic GenAI workflows.

Banking — the broadest. Deutsche Bank in 2023, then Axis Bank, IDFC FIRST, and Revolut India by 2025. The use cases span intelligent automation, agent-to-agent payments infrastructure, and digital-first banking. The deepest banking deployments remain inside large GCCs of global banks rather than Indian-headquartered banks, but the gap is narrowing.

Capital markets and asset management — the most data-rich. Morningstar, Broadridge, Delta Capita in 2023; Motilal Oswal in 2024; MSCI in 2025. The use cases are NLP at scale, document intelligence, research augmentation. This is the sub-sector where the deployment story is least visible publicly — most production systems are internal — but where the financial returns are arguably highest.

Cards and payments — the most operationally embedded. American Express in 2025, Fiserv in 2024, and the broader payments ecosystem in adjacent sessions. The signature deployment pattern is document intelligence — turning the document-heavy workflows of cards processing, dispute resolution, and merchant onboarding into agentic systems.

Fintech infrastructure — the enablers. Perfios in 2023, Snowflake (BFSI vertical) in 2024. The companies that sell to the banks rather than being banks themselves. Their adoption signals are leading indicators of what the banks themselves will deploy 12–18 months later.

Wealth and neo-banking — the newest. Revolut India’s 2025 CEO presence is the strongest signal in this category. Wealthtech and neo-banking have arrived on the Cypher stage; the next two editions will reveal how deep their deployments actually run.

What the maturity arc reveals

Read across the four years, three observations are unmistakable.

One: the BFSI deployment cycle has compressed dramatically. Traditional ML deployments in Indian finance took 3–5 years to move from exploration to production. The GenAI cycle, evidenced through Cypher’s stage, took 18–24 months. The compression is not because banks suddenly became risk-tolerant; it is because the new technology happened to land at a moment when the regulatory and infrastructure preconditions were already in place from the previous decade of ML work.

Two: lending and insurance have outpaced traditional banking. The Indian lending stack (especially in the NBFC and digital-lender categories) and Indian insurance have moved faster than retail banking. This is the opposite of the global pattern, where commercial banks tend to lead. The Indian inversion is worth a separate piece of analysis — it probably reflects the combination of digital-first lenders without legacy debt, and insurance companies under acute pricing pressure that GenAI helps alleviate.

Three: the foreign vs Indian institutional split has narrowed but not closed. Cypher 2023’s BFSI roster was dominated by global captives (Deutsche Bank, Swiss Re, Cigna, Morningstar, Delta Capita). Cypher 2025’s roster is more balanced, with strong Indian institutional representation (AXA India, IDFC FIRST, Axis Bank, Credgenics, Kissht, Yubi). But the depth of production deployment still skews toward global captives. The gap is closing, not closed.

The 2026 question

Cypher 2026’s BFSI agenda will be the most consequential reading of all. If the four-year arc holds, three predictions are reasonable:

First, the number of named production deployments will increase from 23 (2023–2025 cumulative) to roughly 25–30 in the single Cypher 2026 edition. The sector is no longer adopting GenAI selectively; it is doing so structurally.

Second, the dominant 2026 conversation will move from “are we deploying it” to “what is the regulatory framework.” The DPDP Act’s implementation, the RBI’s evolving stance on AI in financial decisioning, and the global wave of AI governance frameworks will all push BFSI conversations toward compliance architecture. The speakers who anchor those sessions will be Chief Risk Officers and Compliance Heads, not Heads of Data Science.

Third, agentic systems will move from session-level discussions to sponsor-level commitments. IDFC FIRST’s 2025 A2A session is a leading indicator. The agentic-platform vendors enabling those deployments — LangChain, Glean, Sierra, and the Indian equivalents now emerging — are likely to appear as Cypher 2026 sponsors. When they do, the BFSI deployment story will have completed its arc from exploration to validation to deployment to commodity infrastructure.

The Cypher stage has, year over year, indexed Indian finance’s GenAI adoption with a precision that no analyst report has matched. The reason is structural: a sector that is forced to disclose, that pays for production failures, and that sends its senior practitioners to one conference each year produces a more honest deployment archive than any vendor-sponsored survey. Twenty-three deployments in three years is the dataset. The pattern is the story.